02. - 05.06.2025

Meet us at the transport logistic in Munich in Hall A5 Booth 234!

Book your appointment now Meet us at the transport logistic in Munich in Hall A5 Booth 234!

02. - 05.06.2025

Search

Top 14 Transpacific Carriers Eastbound Liftings:

May 2018 – Apr 2019

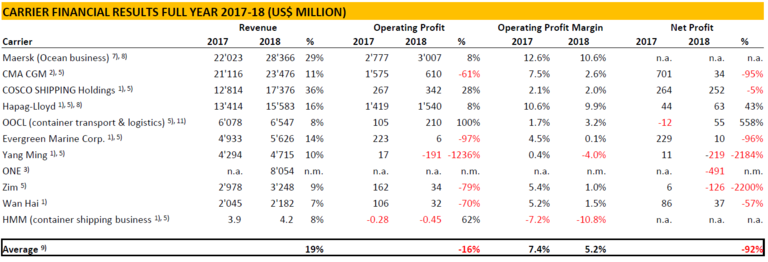

Carrier Results:

Only six of the 11 top carriers who publish their financial results ended in the black, often with marginal net profits.

Reference: ALPHALINER

Please always contact your Gebrüder Weiss Representative to discuss specific ocean rate topic.