02. - 05.06.2025

Meet us at the transport logistic in Munich in Hall A5 Booth 234!

Book your appointment now Meet us at the transport logistic in Munich in Hall A5 Booth 234!

02. - 05.06.2025

Search

IMO 2020 regulation effective 1st January 2020 (International Convention for the Prevention of Pollution from Ships (MARPOL)

IMO 2020 is the first regulation in a series of steps by the International Maritime Organization (IMO) to reduce emissions in response to climate change. IMO2020 requires using fuel with a sulphur content of 0.5 % or lower and will come into effect as of 1st January 2020. Ocean carriers are currently evaluating and testing three options to be compliant with the new regulation:

The spread between HSFO 3.5% and LSFO 0.5% is estimated approximately at USD 250 per ton, while the installation of scrubbers is estimated at about USD 6 – 10 million per vessel. In regards to LNG, shipping lines seem reluctant to use it because of the safety risks.

It is clear that this change will affect the entire shipping industry and the cost of compliance with the new regulation will be significant. The ocean carriers, as well as the forwarders will not be able to absorb these additional costs. At this stage it is not possible to define the exact cost impact. We are in constant dialogue and negotiation with our partner carriers and we will do our outmost to mitigate the impact for our customers.

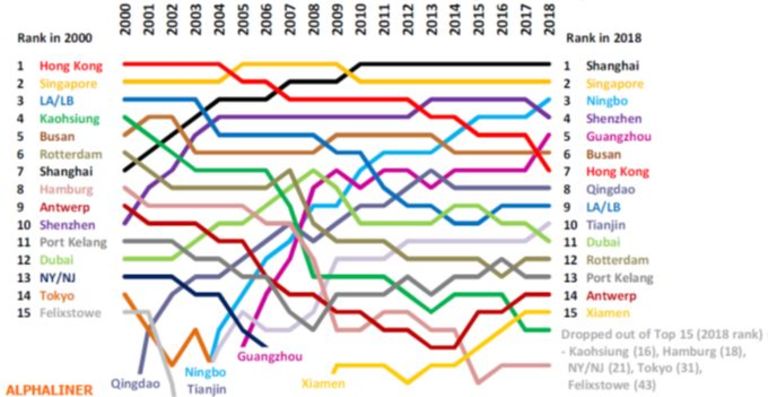

The number of major ports in Asia has climbed from 8 to 11 in 18 years, out of these 11 Asian ports 7 are in China

Reference: ‘ALPHALINER Volume 2019, Issue 1-13’ Please always contact your Gebrüder Weiss Representative to discuss specific ocean rate topic.