02. - 05.06.2025

Meet us at the transport logistic in Munich in Hall A5 Booth 234!

Book your appointment now Meet us at the transport logistic in Munich in Hall A5 Booth 234!

02. - 05.06.2025

Search

The 2M partners MSC and Maersk have launched an Asia – Europe peak season service with the first sailing end of June from Shanghai. Whilst Maersk has announced this service as a kind of ‘sweeper’ operation offering three or four extra sailings in the summer months, MSC has described it as an additional fortnightly loop branded ‘Griffin’ service. The seasonal ‘Griffin’ will only fully materialize if demand growth can sustain it. A 2ndsailing is currently planned for July 5thfrom Shanghai. Maersk and MSC have decided to adopt a flexible approach to offer additional capacity in the summer months to cater for possible peak season volumes and keep their biggest Far East –North Europe loop, the ‘AE-2 / Swan’ service, suspended during Q3.

Hapag-Lloyd responds to increasing Container volume upsurge of its customers. Therefore, we will sail a weekly Far East Loop 4 (FE4) Extra Loader Program for a limited period of four weeks, starting off in week 30 and lasting until week 33. A continuation of this program is dependent on continued demand given the still ongoing global implications of COVID-19.

Maersk and MSC have resumed their joint Far East –USWC ‘TP-8/Orient’ service with sailing of the 13,050 TEU MSC ARIANE on 8 June from Ningbo. The ‘TP-8/Orient’ service is one of the two Transpacific services which were temporarily suspended by 2M in April. Maersk and MSC announced beginning of June that the South East Asia/US East Coast ‘TP-11/Elephant’ service will remain suspended until the end of July. Maersk and MSC are not the only carriers starting to increase their capacity between Asia and the US. The members of THE Alliance announced that five previously cancelled Transpacific voyages were to be reinstated ‘in view of increasing demand’.

| |

Asia to Europe: Carriers are planning a new round of GRI’s for July. The structural blank sailing program is to continue into Q3 to balance out the supply and demand.

Asia to Latin: GRI’s have been announced by carriers from 1stJuly. However, the demand outlook continues to look weak and we do not expect a full GRI amount to be implemented. With the continual demand slack, we are anticipating more blank sailings to follow for the month of July.

Asia to North America: TP market has picked up and the increasing demand level is expected to continue into July. Trade capacity cuts on this trade combined with higher than expected level of demand creates an extremely tight supply-demand balance that continues to push the spot rates. We anticipate spot rates to further increase with July 1stGRI.

Europe to Asia: Space remains super tight on all eastern hemisphere trades due to high amount of blank sailings. PSS and GRI's are still in place and Equipment Imbalance surcharges are still applicable. Rates remain on high level.

North America to Asia: Moderate increase in rates caused by GRI’s. Moderate decline to capacity due to blank sailing.

Asia to Asia: Carriers have announced GRI for IPBC region as of 1stJuly, along with their blank sailings notices. Possibility of full implementation remains bleak as a result of slow market recovery. No huge fluctuation in capacity and freight rates expected in July for Intra Asia. Services are back to normalcy with the easing of COVID-19 restriction in the respective countries.

Asia to Oceania: Capacity is not getting better as of Q3, since Maersk alliance announced the extension of service suspension. The announced GRI in July is expected to push a rate increase of 10-15%. Tight space situation is expected to continue until end of July

| |

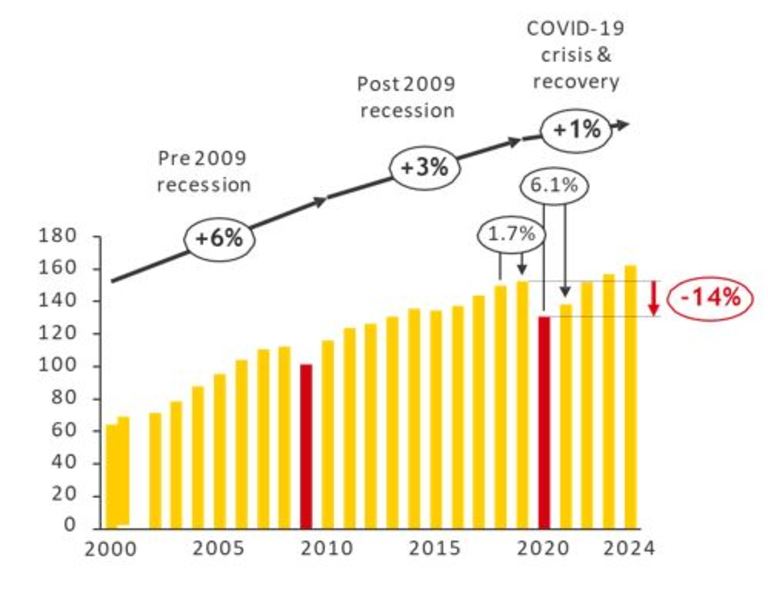

Analysis by Seabury Consulting showed that already before the COVID-19 crises containerized trade grew only modestly by 1.7% in 2019.

Containerized trade is expected to decline by -14% this year, the largest year-on-year decline on record.

In 2021 we will start to see a recovery toward pre-COVID-19-volumes.

Container trade will almost be back at 2019 level in 2022 and is estimated to grow by ~ 3% after that.

Source: Seabury Global Ocean Trade Forecast Database; volume on Y axis in million TEU Growth 2020-20, 2010-19 & 2019-24 measured as CAGR